Complex tax schemes for Exhibitors

Answered

Hall Erickson have an upcoming Exhibition in London. They need to abide by the following guidelines:

---

VAT Guidelines for London:

If Established and Registered in the UK: No VAT will be charged.

Registrants must provide their UK registration number and UK address at the time of registration.

If Not Established or Registered in the UK: VAT at the standard rate of 20% will be charged.

Sponsorships:

Sponsorships are not subject to VAT.

Firms can file for VAT refunds through their local tax authorities, if necessary.

The invoice should indicate “Reverse Charge.”

Exhibitors:

VAT at 20% will be charged.

Registered entities may recover VAT through the normal filing process.

Non-registered entities must use the online refund process.

---

Basically we need to assign different tax rules for Exhibitors in ESC. What is the best approach to facilitate this?

-

Minka Verkaar , Sarah Götza , Maximilian Fankidejski , could you all help provide some guidance on this topic, or know who would be best?

Thanks,

Eric

-

Following

-

Adding Samy Kheloufi and Ryan Ungerboeck as well

-

Adding Clotilda Chuonyo our EMEA finance consultant.

Martin Stephens , could you please provide more details?

In the first paragraph, you mention that registrants with a UK address and UK tax registration are VAT exempt, but in the last paragraph, you state that a 20% VAT is applicable for all exhibitors (including British exhibitors). This seems contradictory.

Additionally, regarding sponsorships: Is the entire invoice VAT exempt under the reverse charge mechanism, or does this apply only to sponsorship items? For example, if a sponsor purchases both a sponsorship package and catering items, would the sponsorship package be VAT exempt with reverse charge, but the catering items subject to 20% VAT since it is not a sponsorship item?

Lastly, what is the ordering process? Is it entirely through ESC, or a mix of back office and ESC? Where should sponsorship packages/items be ordered, ESC or back office? Also, could you clarify who the “Registrants” are? Are they exhibitors ordering from the ESC, or is it something different?

Thanks

-

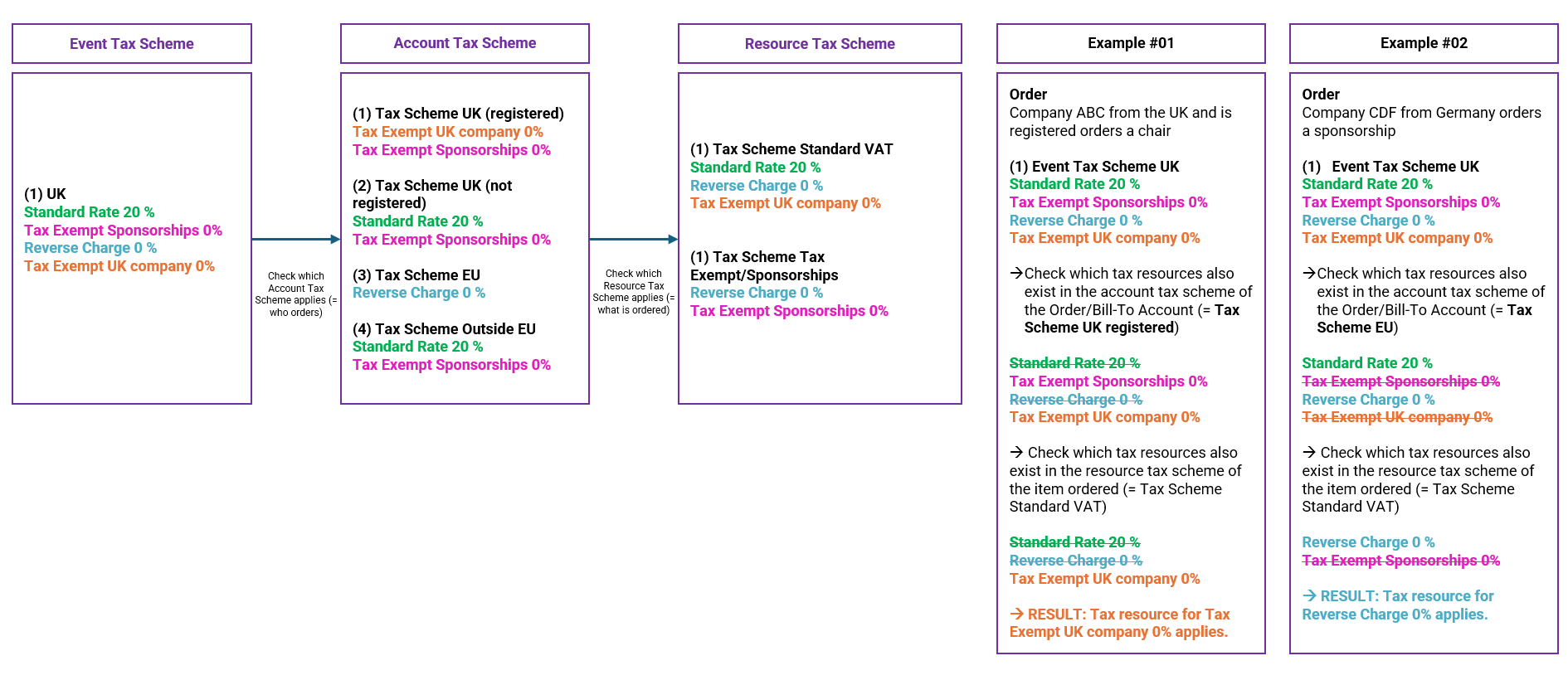

It is a bit difficult to outline it exactly from the given rules, but we would need all 3 levels of tax schemes:

(1) Account Tax Scheme:

- one for UK companies that are requested where no tax applies; we would still set up a tax resource for this scenario labelled “VAT exempt"

- one for UK companies that are sitting in the UK but are not registered/have not provided the registration number and therefore Standard VAT of 20% applies

- one for EU Clients where Reverse Charge applies

- one for any other countries outside where Standard Rate of 20% applies

You can predefine it per country.

(2) Resource Tax Scheme: two schemes are needed at least:

- assuming this already exists for resources they are already selling, the standard VAT tax scheme needs to be modified to include the Standard Rate of 20% as well as the VAT Exempt rate and the Reverse Charge.

- Then either a new Resource Tax Scheme is needed or one is already existing that can be used to manage the Sponsorship items. This tax scheme would typically be just holding the two tax resources for VAT exempt (for UK clients and outside of UK & EU) and the Reverse Charge tax resource for any EU country. Here it is to define for any case where it is not Reverse Charge if a tax line stating Tax Exempt Sponsorship should apply or the standard UK Customer VAT Exempt.

(3) Event Tax Scheme: a new tax scheme for the UK or this particular exhibition needs to be created with all of the above tax resources.

_________

Usually I map it out like this to see if all cases work out, but as mentioned above the Sponsorship items are not clear which rule applies, the rule of the country (UK Tax Exempt vs. Sponsorship items not being subject to VAT):

-

Sarah Götza Samy Kheloufi - your feedback is excellent, the definition of going above and beyond. Sarah, I LOVE your map! Thank you!

I have received clarification on your questions.

- In the first paragraph, it mentions that registrants with a UK address and UK tax registration are VAT exempt, but in the last paragraph, it states that a 20% VAT is applicable for all exhibitors (including British exhibitors). Can you provide clarification?

Provision for exhibition space will be subject to UK VAT to all and any exhibitors. Because provision of land related service is normally exempt, however, INTA opts to tax it (make is subject to VAT), the reverse charge does not apply and VAT applies to all exhibitors. The exhibitors will have the possibility to recover the VAT, those VAT registered in the UK will simply include into their VAT returns, all others have the option to use the refund mechanism. Nobody should be coming to INTA to have the VAT removed / refunded etc

- Additionally, regarding sponsorships: Is the entire invoice VAT exempt under the reverse charge mechanism, or does this apply only to sponsorship items? For example, if a sponsor purchases both a sponsorship package and catering items, would the sponsorship package be VAT exempt with reverse charge, but the catering items subject to 20% VAT since it is not a sponsorship item?

No need to charge VAT on sponsorships. We don’t sell catering items, but I would assume those would have to be charged VAT. We bill for meeting space, not additional items. Catering is sold through the venue.

Sponsorship is in essence advertisement service and for one or another reason, INTA as a foreign (from UK point of view) organization will not be charging UK VAT. Instead, the customers will self account for VAT in the country where they are established. However, this will have nothing to do with INTA or INTA´s invoices.

- Lastly, what is the ordering process? Is it entirely through ESC, or a mix of back office and ESC? "It is a Mix". Where should sponsorship packages/items be ordered, ESC or back office? “Backoffice”. Also, could you clarify who the “Registrants” are? Are they exhibitors ordering from the ESC, or is it something different? "Exhibitors"

Your feedback has opened an opportunity for a Professional Services engagement with this client, which I am currently exploring with the account manager.

-

Fantastic! I love the swift identification of opportunities.

Based on the shared data, I am confident that Enterprise can effectively meet all customer requirements. However, additional professional services will be necessary to ensure all requirements are thoroughly identified and to design the necessary configurations.

Please sign in to leave a comment.

Comments

7 comments

Date Votes